Obtaining Fintech Licences Workflow: Step-by-Step Guide

- NUR Legal

- Dec 7, 2025

- 7 min read

Nearly 80 percent of British fintech startups face regulatory challenges before they even launch. Getting the right licence is not just a legal obligation but a vital step for gaining trust and tapping into global growth. With rules constantly changing and each licence carrying unique requirements, British founders need practical guidance to map their business needs and meet compliance from the very beginning.

Table of Contents

Quick Summary

Key Insight | Explanation |

1. Assess Business Needs First | Understand your precise financial offerings and select the right licence type based on your operational model and target markets. |

2. Prepare Documentation Thoroughly | Develop a detailed portfolio, including compliance policies and internal procedures, to showcase your regulatory readiness. |

3. Submit Well-Organised Applications | Organise your documentation logically and ensure compliance with submission guidelines for a successful application. |

4. Communicate Effectively with Regulators | Engage with regulators during the review process, providing timely and accurate responses to any inquiries they may have. |

5. Maintain Compliance Post-Issuance | After obtaining your licence, implement rigorous compliance strategies and regular audits to uphold regulatory standards. |

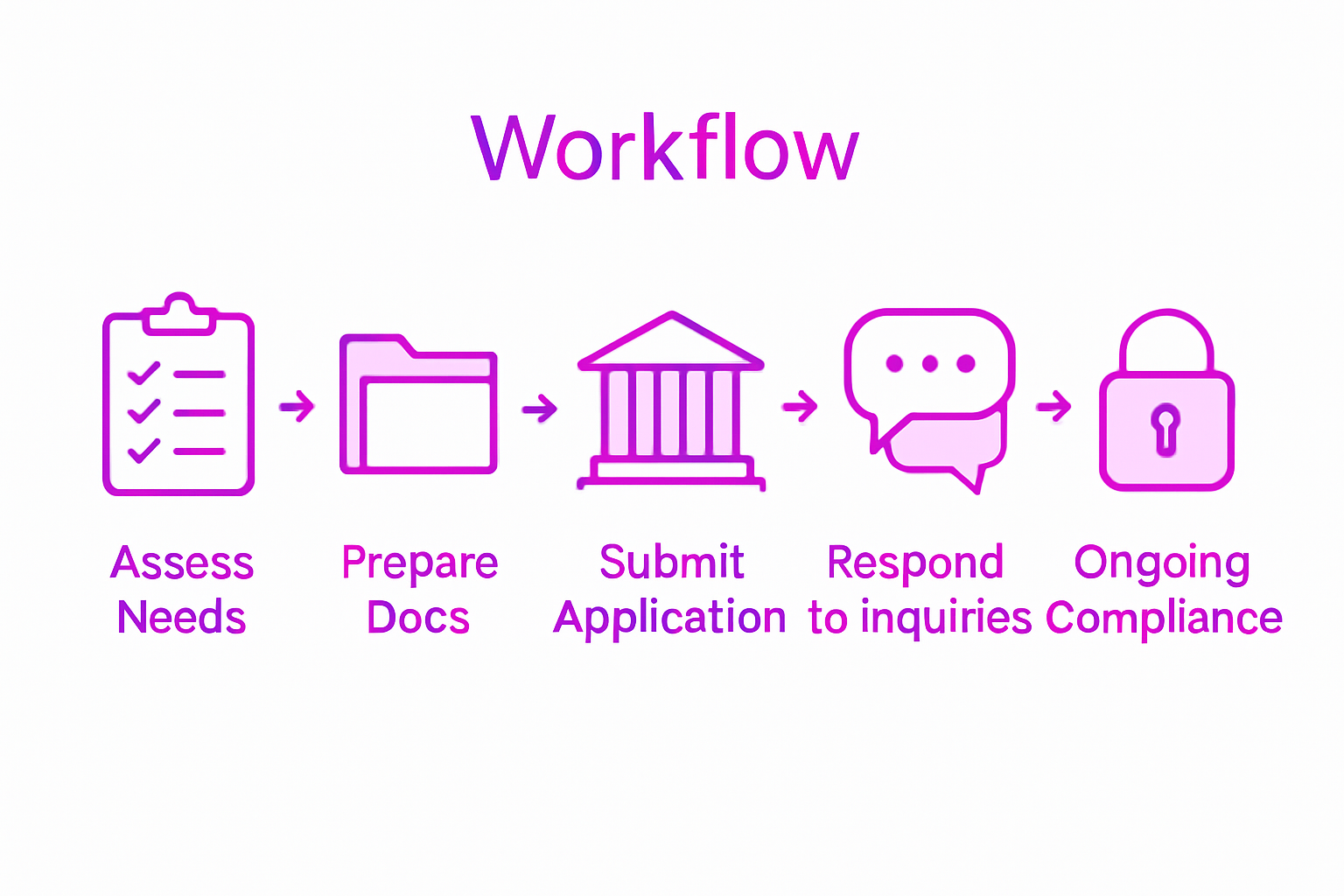

Step 1: Assess Business Needs and Licensing Options

Successfully obtaining a fintech licence begins with a comprehensive assessment of your specific business requirements and operational model. This critical first stage involves understanding your precise financial service offerings and matching them with the most appropriate regulatory framework.

Your initial focus should involve carefully mapping your business operations against potential licensing categories. Different licence types cater to unique business models such as Payment Institution (PI), Electronic Money Institution (EMI), or Payment Service Provider (PSSP). Consider your intended financial services, target markets, transaction volumes, and geographical scope. Will you process digital payments? Provide electronic money services? Facilitate cross-border transactions? Each activity requires specific regulatory recognition and compliance protocols.

One strategic recommendation is to conduct a thorough internal audit of your planned financial services. Document every proposed transaction type, anticipated customer interaction, and potential revenue stream. This granular approach helps regulators understand your business model and streamlines the licensing application process. Pro tip: Engage legal specialists who understand international financial regulations to help you navigate complex licensing requirements.

By meticulously assessing your business needs upfront, you create a solid foundation for selecting the right licence category and demonstrating regulatory compliance. Your next step will involve preparing a comprehensive application package tailored to your specific operational model.

Step 2: Prepare Required Documentation and Compliance Policies

Preparing comprehensive documentation and robust compliance policies is a critical phase in securing your fintech licence. This step involves assembling a detailed portfolio that demonstrates your business’s regulatory readiness and operational integrity.

Your documentation process should start with developing comprehensive internal procedures that address key regulatory requirements. This includes crafting meticulous Anti-Money Laundering (AML) and Know Your Customer (KYC) policies that showcase your commitment to financial transparency. You will need to compile a robust business plan, detailed financial projections, organisational structure, and comprehensive compliance frameworks that illustrate your understanding of regulatory expectations.

A strategic approach involves creating a systematic documentation checklist. Ensure you include essential elements such as proof of initial capital, detailed business model descriptions, risk management strategies, and governance protocols. Regulatory bodies will scrutinise these documents carefully, so precision and thoroughness are paramount. Pro tip: Consider engaging a legal specialist who can review your documentation to ensure it meets the specific requirements of your target jurisdiction.

By methodically preparing these critical documents, you establish a strong foundation for your licence application. The next phase will involve submitting your meticulously compiled documentation package to the relevant regulatory authorities.

Step 3: Submit Legal Applications to Regulatory Authorities

Submitting your legal application is a pivotal moment in your fintech licensing journey. This critical stage transforms your carefully prepared documentation into an official regulatory submission that will determine your business’s operational future.

Navigating the application submission process requires meticulous attention to detail and strategic preparation. Each regulatory authority will have specific requirements for document formatting, supplementary evidence, and submission protocols. Ensure you thoroughly review the specific guidelines of your target jurisdiction. Typically, your application package will need to demonstrate robust financial stability, comprehensive compliance frameworks, and a clear operational strategy.

Careful organisation is paramount when compiling your submission. Arrange all documents in a logical sequence, cross reference supporting materials, and include precise contact information for follow up. Pro tip: Create digital and physical copies of your entire application set and maintain a detailed tracking log of every document submitted. Some regulatory bodies may require additional certifications or translations of key documents.

By presenting a comprehensive, well structured application, you significantly improve your chances of securing the required licence. The subsequent phase will involve awaiting initial regulatory review and potentially responding to any supplementary information requests.

Step 4: Respond to Regulator Inquiries and Provide Clarifications

Engaging with regulatory authorities represents a critical phase in your fintech licensing journey. This stage demands precision, professionalism, and strategic communication to successfully navigate potential queries and demonstrate your operational readiness.

Maintaining open communication channels with regulatory bodies is fundamental to your licence application process. When regulators request additional information or seek clarification, your response must be timely, comprehensive, and meticulously structured. Prepare a dedicated team or point of contact who understands the intricate details of your application and can respond with technical accuracy and professional demeanour.

Develop a systematic approach to handling regulatory inquiries. Create a comprehensive response template that allows for rapid yet thorough communication. Ensure all responses are well documented, include precise references to original application materials, and directly address each specific point raised by the regulatory authority. Pro tip: Maintain a detailed log of all communications, including dates, specific queries, and your corresponding responses. This documentation will serve as a critical reference and demonstrate your commitment to transparency.

By responding efficiently and professionally to regulatory inquiries, you significantly enhance your prospects of securing the desired fintech licence. The subsequent phase will involve awaiting final regulatory assessment and potential licence approval.

Step 5: Verify Issuance and Maintain Ongoing Compliance

Obtaining your fintech licence marks the beginning of a continuous regulatory journey. This crucial stage requires meticulous attention to detail and proactive management of your regulatory obligations.

Implementing robust compliance strategies is fundamental to sustaining your operational legitimacy. Upon receiving your official licence, conduct a comprehensive verification process to ensure all documentation matches the regulatory specifications. Your ongoing compliance framework should include systematic internal audits, regular policy reviews, and continuous monitoring of regulatory updates that might impact your business operations.

Establish a dedicated compliance team responsible for tracking and implementing regulatory requirements. This team should develop a dynamic compliance calendar that schedules periodic reviews, reporting deadlines, and mandatory documentation updates. Pro tip: Create a centralised digital repository for all regulatory documents, enabling rapid access and efficient management of compliance evidence. Maintain meticulous records of all interactions, submissions, and internal policy modifications to demonstrate your commitment to transparency and regulatory adherence.

By maintaining rigorous ongoing compliance, you protect your business from potential regulatory penalties and position yourself as a credible operator in the fintech ecosystem. The next phase involves continuous learning and adaptation to the evolving regulatory landscape.

Simplify Your Fintech Licensing Journey with Expert Legal Support

Navigating the complex workflow of obtaining fintech licences requires precise planning, meticulous documentation, and clear communication with regulatory authorities. The step-by-step guide highlights challenges such as assessing your business model, preparing detailed AML and KYC policies, and managing ongoing compliance. At NUR Legal, we understand these pain points and offer tailored legal consultancy to streamline every phase of your licence application process. Whether you are launching a Payment Institution or aiming for an Electronic Money Institution licence, our expertise ensures your operations align fully with regulatory demands.

Start securing your fintech licence today by partnering with specialists who deliver clarity, efficiency, and trust. Visit NUR Legal to explore how our global licensing solutions and compliance services can accelerate your approval. For deeper insight into regulatory compliance and application support, check our detailed Fintech Licensing Guide and connect with experts ready to assist. Don’t delay your growth in this highly regulated ecosystem. Contact us now at https://nur-legal.com and turn complex legal challenges into competitive advantages.

Frequently Asked Questions

What are the initial steps for obtaining a fintech licence?

Successfully obtaining a fintech licence begins with assessing your business needs and identifying the appropriate licensing options. To start, map your business operations against potential licence categories, such as Payment Institution or Electronic Money Institution, based on your specific financial service offerings.

What documentation is required for the licensing application?

For the licensing application, you need comprehensive documentation, including Anti-Money Laundering and Know Your Customer policies, a detailed business plan, and financial projections. Prepare a checklist to ensure you compile all essential documents like proof of initial capital and governance protocols before submission.

How do I respond to regulatory inquiries during the licensing process?

To handle regulatory inquiries effectively, maintain open communication with regulatory authorities and prepare timely, thorough responses to their requests. Create a response template that references your original application materials to ensure clarity and address each specific query adequately.

How can I verify the issuance of my fintech licence?

After receiving your fintech licence, conduct a comprehensive verification to ensure that all documentation aligns with regulatory specifications. Establish a dedicated compliance team to manage ongoing obligations and perform regular internal audits.

What ongoing compliance measures should I implement post-licensing?

Implementing robust compliance strategies is crucial after obtaining your fintech licence. Develop a dynamic compliance calendar to track periodic reviews and maintain detailed records of all interactions and submissions to demonstrate adherence to regulatory requirements.

Recommended

Comments