Role of Regulators in Fintech – Safeguarding Innovation and Trust

- NUR Legal

- Dec 19, 2025

- 7 min read

Every British fintech startup faces the challenge of rapid innovation alongside ever-shifting regulations. With more than 60 percent of European fintech companies listing compliance as a top concern, understanding the role of regulators is crucial. This topic matters because strong oversight shapes the future of financial services, consumer trust, and market stability. Discover what makes regulatory bodies so influential in guiding responsible growth and protecting both markets and consumers.

Table of Contents

Key Takeaways

Point | Details |

Role of Regulators | Regulators are essential in creating frameworks that balance consumer protection with technological innovation in the fintech sector. |

Proactive Compliance | Engaging with regulatory frameworks early can streamline compliance and mitigate legal risks for fintech organisations. |

Diverse Regulatory Landscape | Different jurisdictions have varying regulatory approaches, requiring firms to adapt their strategies accordingly. |

Risk Management | Developing robust internal controls and risk assessment strategies is crucial for navigating complexities and avoiding enforcement actions. |

Defining the Role of Regulators in Fintech

Financial technology (fintech) represents a dynamic ecosystem where innovation intersects with complex regulatory challenges. Regulators play a critical function in establishing structured frameworks that protect consumers, maintain financial stability, and promote responsible technological advancement. Financial regulation provides essential oversight to manage risks inherent in emerging financial technologies.

The primary responsibilities of fintech regulators extend beyond traditional monitoring. They must balance encouraging technological innovation with protecting stakeholder interests. This nuanced approach involves creating adaptive frameworks that can respond quickly to technological changes while maintaining robust safeguards. Regulatory bodies establish comprehensive guidelines that address critical areas such as data protection, cybersecurity, consumer rights, and financial transparency.

At the core of regulatory intervention are several key objectives. These include preventing financial fraud, ensuring fair market competition, protecting consumer data privacy, and mitigating systemic risks that could potentially destabilise financial markets. Structured regulatory frameworks help fintech companies operate within legal parameters, providing clear guidelines while supporting responsible innovation.

Pro Tip for Entrepreneurs: Proactively engage with regulatory frameworks by developing comprehensive compliance strategies before launching financial technology products. Understanding regulatory requirements early can save significant time and resources in the long term.

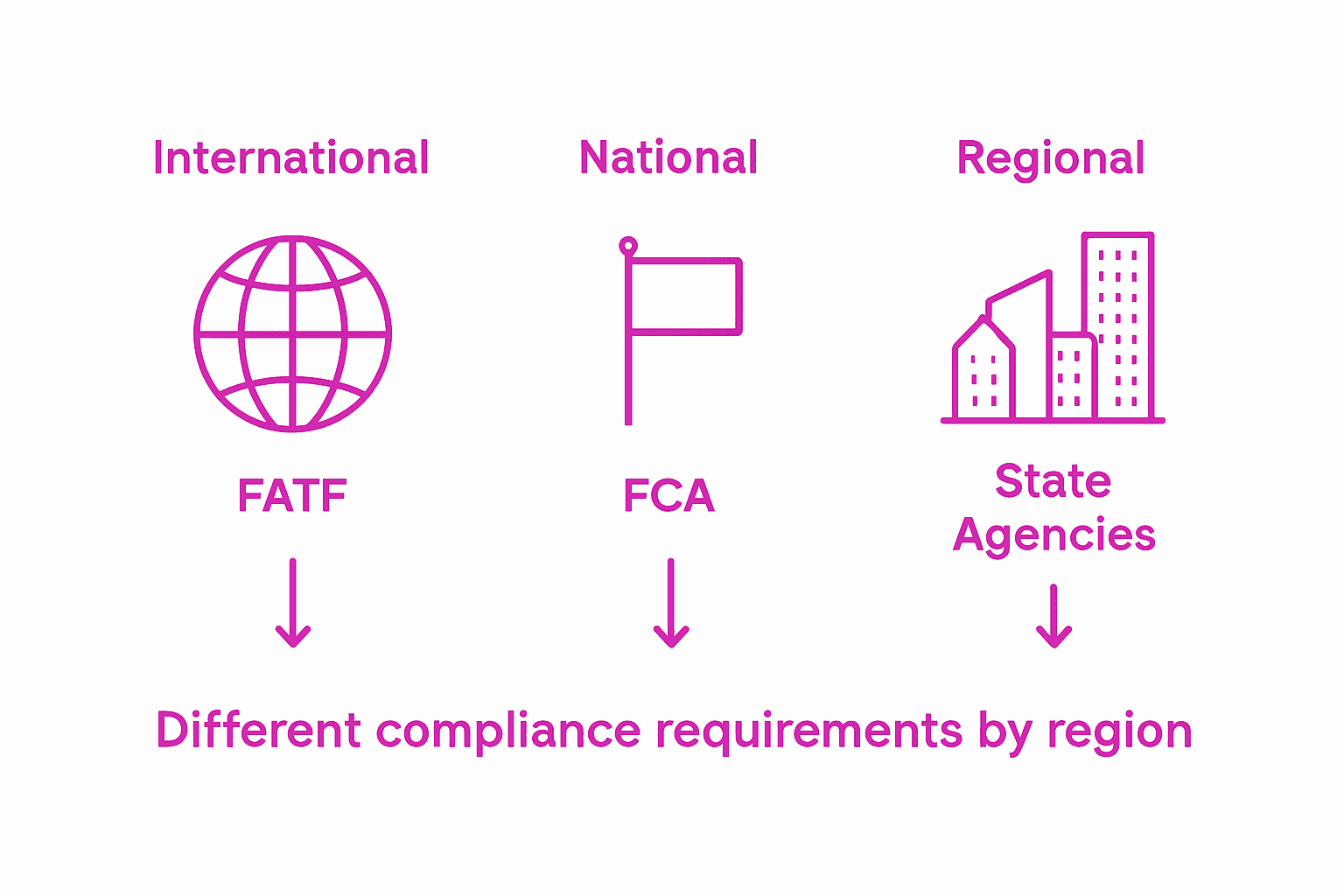

Types of Regulatory Bodies and Jurisdictions

Financial regulatory bodies operate across multiple levels, ranging from international organisations to national and regional authorities. The Basel Committee on Banking Supervision represents a critical international regulatory framework that coordinates supervisory standards and promotes global financial stability. These international bodies establish baseline guidelines that national regulators then adapt to their specific economic contexts.

National regulatory authorities play a pivotal role in overseeing financial technology ecosystems within their jurisdictions. Regulatory agencies like the Swiss Financial Market Supervisory Authority (FINMA) demonstrate how specialised governmental bodies can effectively monitor diverse financial sectors including banking, insurance, and emerging technological platforms. These national regulators develop targeted frameworks that address unique market characteristics while maintaining alignment with international standards.

The complexity of regulatory landscapes requires businesses to understand jurisdiction-specific requirements. Different regions implement varying approaches to fintech oversight, with some adopting more progressive, innovation-friendly models while others maintain stricter control mechanisms. Key regulatory bodies include central banks, financial conduct authorities, securities and exchange commissions, and specialised fintech oversight departments that collectively ensure market integrity and consumer protection.

Here is a summary of primary regulatory bodies and their distinctive roles in fintech regulation:

Level | Example Body | Main Focus | Relevance to Fintech |

International | Basel Committee on Banking Supervision | Setting global banking standards | Promotes stability and best practices |

National | Swiss Financial Market Supervisory Authority (FINMA) | Supervising banks, fintech, insurance | Enforces country-specific compliance |

Regional | European Banking Authority | Harmonising regulations across Europe | Fosters cross-border fintech adoption |

Specialised | Fintech Regulatory Sandboxes | Testing innovative solutions legally | Supports responsible innovation |

Pro Tip for Compliance Officers: Develop a comprehensive regulatory mapping strategy that tracks legislative changes across multiple jurisdictions, enabling proactive adaptation to evolving compliance requirements and minimising potential legal risks.

Legal Frameworks Shaping Fintech Regulation

Legal frameworks for fintech regulation represent complex systems designed to address the dynamic challenges of technological innovation in financial services. Understanding fintech regulation requires comprehensive insight into the evolving legal landscape that balances technological advancement with consumer protection and market stability. These frameworks comprise interconnected layers of legislation, regulatory guidelines, and compliance requirements that adapt to emerging technological trends.

Regulatory compliance involves multiple dimensions, including data protection, cybersecurity, financial transparency, and consumer rights. Different jurisdictions develop nuanced approaches to managing financial technologies, creating a patchwork of regulatory models that businesses must navigate carefully. Key legal considerations include anti-money laundering (AML) protocols, know-your-customer (KYC) requirements, capital adequacy standards, and frameworks for managing digital financial transactions.

The legal landscape for fintech is characterised by continuous evolution, with regulatory bodies constantly updating guidelines to address emerging technological risks and opportunities. Innovative financial technologies such as blockchain, cryptocurrency, peer-to-peer lending platforms, and digital payment systems challenge traditional regulatory paradigms, requiring flexible and adaptive legal frameworks that can respond to rapid technological changes while maintaining market integrity and protecting stakeholder interests.

Pro Tip for Legal Professionals: Develop a proactive regulatory intelligence strategy that monitors legislative changes across multiple jurisdictions, enabling anticipatory compliance and minimising potential legal vulnerabilities for financial technology enterprises.

Core Compliance and Reporting Requirements

Financial technology enterprises must navigate a complex landscape of compliance and reporting obligations that extend far beyond traditional regulatory checkboxes. Fintech platforms’ reputations are critically influenced by regulatory perceptions and transparent reporting practices, requiring organisations to develop sophisticated and comprehensive compliance strategies that demonstrate commitment to ethical and legal standards.

Reporting requirements encompass multiple critical dimensions, including financial transparency, transaction monitoring, risk management, and detailed documentation of operational processes. Key compliance elements involve implementing robust anti-money laundering (AML) protocols, conducting rigorous know-your-customer (KYC) assessments, maintaining precise financial records, and providing regular detailed reports to relevant regulatory authorities. Complex algorithmic systems in fintech demand stringent compliance with transparency and accountability standards, ensuring fair and ethical decision-making processes that protect both consumers and financial institutions.

The regulatory landscape for fintech compliance is dynamic and multifaceted, requiring organisations to continuously adapt their reporting mechanisms. This involves developing sophisticated technological infrastructures capable of real-time monitoring, automated compliance checking, and comprehensive documentation. Successful compliance strategies integrate advanced data analytics, machine learning algorithms, and proactive risk assessment tools to create comprehensive regulatory frameworks that can efficiently manage the complex challenges of modern financial technologies.

The following table compares common compliance challenges faced by fintech firms and suggested strategies to address them:

Compliance Challenge | Example in Fintech | Impact on Business | Mitigation Strategy |

AML & KYC Standards | Onboarding digital clients | Regulatory penalties | Automate identity verification |

Data Protection | Handling client information | Loss of customer trust | Implement encryption measures |

Real-time Reporting | Instant payment platforms | Fines for late filings | Employ automated audit tools |

Algorithmic Transparency | Credit scoring algorithms | Accusations of bias | Regular transparency reviews |

Pro Tip for Compliance Managers: Implement an integrated compliance management system that combines automated monitoring, continuous staff training, and periodic independent audits to maintain a proactive and adaptive approach to regulatory requirements.

Risks, Liabilities, and Enforcement Actions

Financial technology organisations operate within a complex regulatory environment where risks, liabilities, and potential enforcement actions represent critical considerations for sustainable business operations. Regulatory sandboxes provide controlled environments for managing innovation-related risks, enabling financial institutions to test novel technologies under carefully monitored conditions that balance technological advancement with regulatory compliance.

Legal liability in fintech encompasses multiple dimensions, including potential financial penalties, reputational damage, and regulatory sanctions. Enforcement actions can range from monetary fines and operational restrictions to complete licence revocations, depending on the severity of regulatory breaches. Key risk areas include data protection violations, inadequate anti-money laundering (AML) protocols, insufficient know-your-customer (KYC) procedures, cybersecurity vulnerabilities, and non-transparent algorithmic decision-making processes. Regulatory bodies like the China Banking and Insurance Regulatory Commission demonstrate how comprehensive supervisory frameworks can effectively manage institutional risks through systematic monitoring and targeted enforcement mechanisms.

Navigating the intricate landscape of regulatory risks requires financial technology enterprises to develop proactive compliance strategies. This involves implementing robust internal control systems, conducting regular risk assessments, maintaining comprehensive documentation, and establishing transparent communication channels with regulatory authorities. Successful risk management integrates technological solutions such as advanced analytics, machine learning algorithms, and real-time monitoring tools to identify and mitigate potential compliance vulnerabilities before they escalate into significant legal challenges.

Pro Tip for Risk Managers: Develop a dynamic risk assessment framework that combines continuous technological monitoring, periodic external audits, and adaptive compliance protocols to stay ahead of emerging regulatory challenges and minimise potential enforcement risks.

Navigate Fintech Regulation with Confidence and Expert Support

The article highlights how fintech businesses face intricate regulatory challenges requiring a balanced approach to innovation and compliance. Navigating evolving legal frameworks, managing AML and KYC obligations, and responding to cross-jurisdictional requirements can be overwhelming without specialised guidance. Key pain points include adapting to dynamic compliance demands while maintaining consumer trust and avoiding costly enforcement actions.

At NUR Legal, we understand these challenges intimately. Our expert team offers tailored solutions for fintech companies seeking to establish and maintain legally compliant operations globally. From securing essential licences such as crypto and gaming permits to providing comprehensive legal opinions and contract reviews, we empower your business to meet rigorous regulatory standards with confidence. Benefit from our strong relationships with regulators across multiple jurisdictions and our commitment to transparency, efficiency, and affordable service.

Partnering with us means you gain a trusted legal ally dedicated to helping you manage compliance complexities and safeguard innovation. Don’t let regulatory risks stall your fintech venture. Explore how our professional consultancy can support your success today by visiting NUR Legal.

Start securing your fintech future now – connect with NUR Legal to transform regulatory challenges into competitive advantages. Visit us at https://nur-legal.com for expert corporate, licensing, and compliance support tailored specifically for your fintech business.

Frequently Asked Questions

What is the role of regulators in the fintech industry?

Regulators in the fintech industry establish structured frameworks to protect consumers, maintain financial stability, and promote responsible innovation. They ensure compliance with laws and regulations that govern financial technologies.

How do regulatory bodies balance innovation and consumer protection?

Regulatory bodies strive to create adaptive frameworks that respond to technological changes while safeguarding consumer interests. They encourage innovation by establishing clear guidelines that fintech companies must follow to protect stakeholders.

What are the key compliance requirements for fintech firms?

Key compliance requirements for fintech firms include implementing anti-money laundering (AML) protocols, conducting know-your-customer (KYC) assessments, ensuring data protection, and maintaining transparency in financial reporting.

What risks do fintech companies face from regulatory enforcement?

Fintech companies can face risks such as monetary penalties, reputational damage, and operational restrictions as a result of regulatory enforcement actions. Common areas of risk include data protection violations and inadequate compliance with AML and KYC standards.

Recommended

Comments