What Is KYC in Fintech: Safeguarding Compliance and Trust

- NUR Legal

- Jan 22

- 14 min read

Securing proper licensing for a fintech or crypto startup often feels like an obstacle course, especially when KYC requirements are poorly understood. For founders and compliance officers, Know Your Customer (KYC) is the foundation of regulatory approval and operational trust. Each licensing authority, whether in Georgia, Seychelles, or the United Kingdom, expects rigorous systems for identity verification, risk assessment, and ongoing monitoring. This guide breaks down the core KYC processes and why thorough implementation is critical for fintech success.

Table of Contents

Key Takeaways

Point | Details |

Understanding KYC Components | Familiarise with the three core components—CIP, CDD, and EDD—to structure a comprehensive KYC framework that meets regulatory expectations. |

Automation and Technology | Leverage AI-driven technology for KYC processes to enhance efficiency, reduce costs, and improve customer onboarding experiences. |

Regulatory Compliance | Stay informed about varying KYC regulations across jurisdictions to ensure compliance and mitigate risks associated with non-compliance. |

Ongoing Monitoring | Implement continuous monitoring of customer transactions to adapt risk assessments and quickly address suspicious activities. |

KYC in Fintech: Definition and Core Purpose

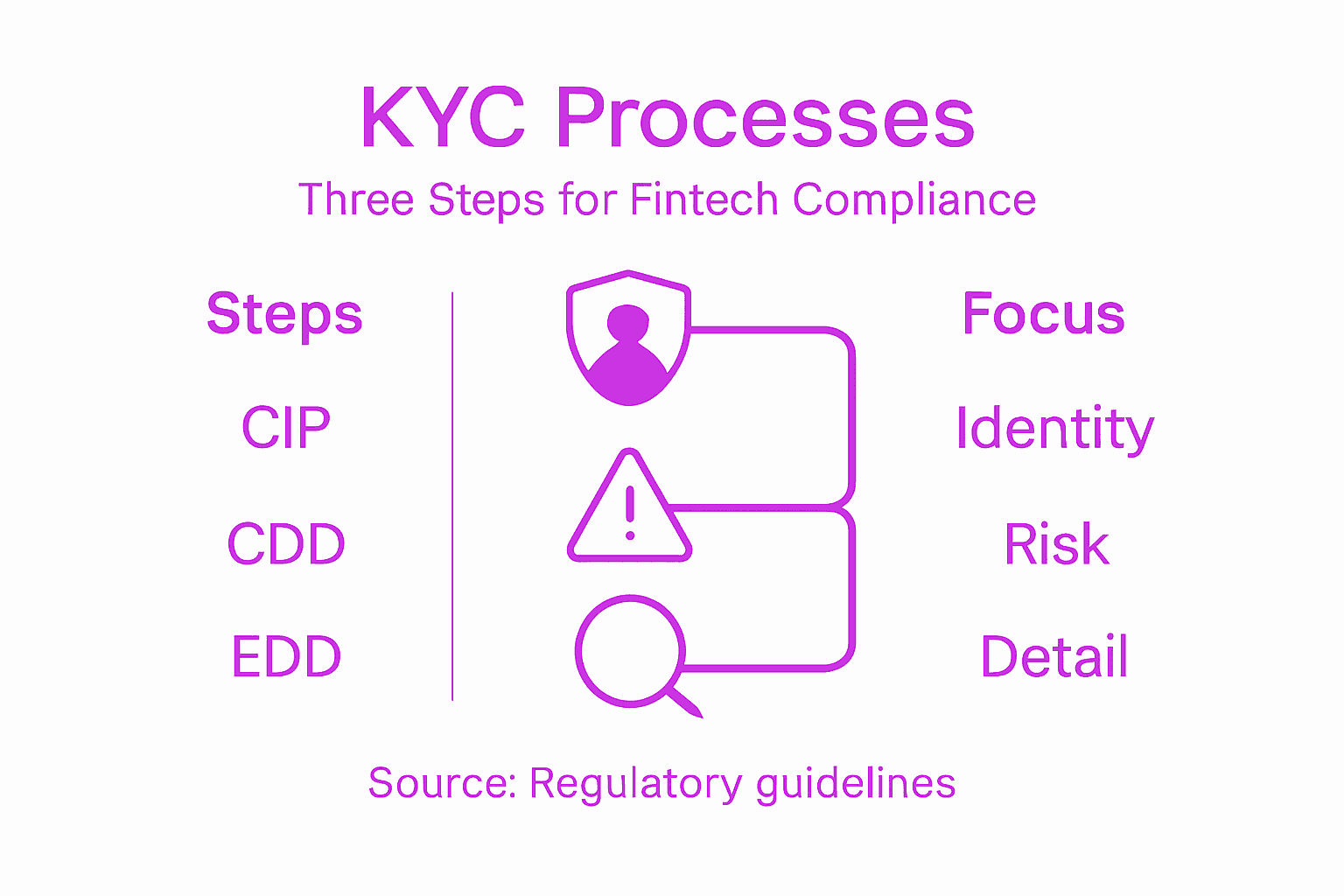

Know Your Customer (KYC) sits at the heart of fintech compliance, yet many founders misunderstand what it actually entails. At its core, KYC represents a multi-step verification process that financial institutions use to confirm customer identities before providing services. Think of it as the gatekeeping mechanism that separates legitimate operations from those exposed to fraud, money laundering, and terrorist financing. For fintech startups seeking licensing in jurisdictions like Georgia or Seychelles, understanding KYC isn’t optional—it’s foundational to obtaining and maintaining regulatory approval. The process involves three interconnected components: Customer Identification Program (CIP), which verifies who your customers actually are; Customer Due Diligence (CDD), which assesses the risk profile of those customers; and Enhanced Due Diligence (EDD), which applies stricter scrutiny to high-risk clients.

What separates effective KYC from compliance theatre is genuine risk assessment. Your business doesn’t simply collect identification documents and tick a box. Instead, KYC requires you to understand the purpose and nature of each customer relationship, scrutinise the source of funds, and continuously monitor transactions against regulatory watchlists. When regulators in Curaçao or Anjouan evaluate your gaming or fintech licence application, they examine whether your KYC framework actually prevents criminals from using your platform. The mechanics have transformed dramatically with technology. Identity verification now uses AI and biometrics to accelerate customer onboarding whilst maintaining rigorous security standards, though the underlying principle remains unchanged: confirm identity, assess risk, and document everything.

For compliance officers at crypto startups, the stakes are particularly high. Regulatory bodies treat cryptocurrency businesses with heightened scrutiny precisely because they’ve historically lacked robust KYC safeguards. Your KYC programme must demonstrate that you can identify beneficial owners of wallets, understand transaction flows, and flag suspicious activity in real time. The difference between a startup that obtains its Seychelles crypto licence smoothly and one that faces enforcement actions often comes down to how thoroughly KYC was embedded into operations from day one. The role of compliance in fintech extends far beyond KYC alone, but KYC forms the foundation upon which every other control rests. When you onboard a customer, you’re not just collecting data—you’re creating an audit trail that proves your business exercised reasonable diligence to prevent financial crime.

Pro tip: Build your KYC process with regulatory reporting in mind from the start. Collect only the data fields you’ll actually need for risk assessment and compliance documentation, avoiding the bloat that slows onboarding and creates security vulnerabilities.

Types of KYC Processes in Fintech

KYC operates through three distinct but interconnected processes, each serving a specific purpose in your compliance framework. Customer Identification Program (CIP) forms the foundation, requiring you to verify a customer’s identity using official documents such as passports, driving licences, or national identity cards. In digital environments, biometric verification such as facial recognition has become increasingly common, allowing you to confirm identity without requiring physical presence. CIP is straightforward in principle but demands rigorous execution because it creates the baseline record against which all future transactions are evaluated. When your fintech startup applies for licensing in Georgia or handles gaming operations in Curaçao, regulators examine whether your CIP process actually prevents false identities from entering your system.

Customer Due Diligence (CDD) moves beyond simple identity verification into risk assessment. Here you investigate the purpose and nature of the customer relationship, examine their financial background, and establish ongoing monitoring protocols. CDD requires understanding where customer funds originate, what industries they operate in, and whether their transaction patterns match their stated business purpose. For instance, if a customer claims to be a freelance translator but submits deposits of £500,000 monthly from shell companies registered in high-risk jurisdictions, CDD should trigger investigation before you proceed. The KYC process includes verification using official documents or biometrics during identification, but CDD demands active analysis of that customer’s financial behaviour. This distinction matters enormously when regulators review your files. They want evidence that you thought critically about risk, not just that you collected documentation.

Enhanced Due Diligence (EDD) represents the highest level of scrutiny, applied to customers identified as higher risk through your CDD assessment. High-risk profiles include politically exposed persons (PEPs), customers from jurisdictions subject to international sanctions, individuals with known connections to financial crime, or those conducting unusual transaction volumes. EDD requires additional documentation, verification of beneficial ownership structures, ongoing transaction monitoring, and potentially periodic re-verification of identity. For crypto startups seeking Seychelles licensing, EDD becomes critical because regulators expect you to understand who ultimately controls each wallet and why they’re transacting on your platform. The cost and effort of EDD should motivate you to tier your customer base appropriately, applying standard CDD to low-risk customers whilst reserving intensive scrutiny for genuinely suspicious activity.

The interplay between these three processes creates your complete KYC framework. CIP establishes who the customer is. CDD determines their risk profile. EDD ensures that high-risk customers receive proportionate scrutiny. When establishing regulatory compliance for your fintech startup, you must document clear decision trees showing when each process applies, who within your organisation makes risk determinations, and how you escalate suspicious findings to your compliance team. Variation by jurisdiction and industry means that a gaming operation in Anjouan may require different CDD thresholds than a cryptocurrency exchange in Seychelles, but the underlying logic remains consistent: verify identity, assess risk, monitor continuously.

Here is a summary showing how the three core KYC components differ in focus and impact:

KYC Component | Main Focus | Application Timing | Example of Business Impact |

CIP (Customer Identification Programme) | Identity verification | Onboarding/start of relationship | Prevents fake identities entering system |

CDD (Customer Due Diligence) | Risk profile assessment | Ongoing, especially for higher risk | Detects unusual transaction patterns |

EDD (Enhanced Due Diligence) | In-depth scrutiny for high risk | As triggered by CDD findings | Filters out money laundering attempts |

Pro tip: Automate your CIP and routine CDD screening using integrated identity verification platforms, then reserve your compliance team’s effort for EDD investigations and edge-case decisions where human judgment genuinely adds value.

Legal Frameworks and Regulatory Obligations

KYC operates within a complex web of international, regional, and local legal frameworks that your fintech startup must navigate. The Financial Action Task Force (FATF) establishes global standards that most countries adopt, creating baseline requirements for customer identification, risk assessment, and suspicious activity reporting. However, FATF guidance alone doesn’t tell the full story. Individual jurisdictions layer their own requirements on top, meaning that a crypto startup operating in Seychelles faces different specific obligations than one in Georgia, even though both must ultimately satisfy FATF principles. The Financial Conduct Authority (FCA) in the United Kingdom imposes stringent KYC procedures tailored to the UK’s regulatory environment, whilst the European Union’s Anti-Money Laundering Directives create obligations across all member states. Understanding these frameworks isn’t academic exercise. Non-compliance triggers severe consequences including hefty fines, licence revocation, and reputational damage that can destroy a startup before it generates meaningful revenue.

For fintech companies in regulated sectors, Anti-Money Laundering (AML) and KYC obligations are inseparable. The US Bank Secrecy Act and the USA PATRIOT Act mandate that American fintechs verify customer identities, conduct enhanced due diligence on high-risk clients, report suspicious activities through Suspicious Activity Reports (SARs), and file beneficial ownership disclosures. The European Union’s Sixth AML Directive creates parallel requirements across Europe. AML and KYC regulations require customer identification and risk-based assessments to prevent fraud and money laundering across jurisdictions. When you submit a licensing application in Curaçao for gaming operations or in Anjouan, regulators examine whether your procedures align with both FATF standards and local implementing legislation. This dual compliance burden means you cannot simply copy another company’s KYC programme. Your procedures must be tailored to your specific business model, customer base, and the jurisdictions where you operate.

The practical reality for compliance officers is that regulatory requirements vary substantially by customer type and transaction volume. A customer receiving a single £1,000 wire transfer receives different scrutiny than someone conducting £500,000 in daily cryptocurrency transactions. Risk-based approaches allow you to apply proportionate controls, investing intensive effort in genuinely suspicious activity rather than creating bureaucratic burden for low-risk customers. Your KYC framework must document these risk tiers explicitly, showing regulators that you’ve thought carefully about proportionality. For crypto startups seeking Seychelles licensing, this means demonstrating that your enhanced due diligence procedures for high-risk wallets exceed standard procedures proportionately. Sanctions screening is mandatory for all jurisdictions, requiring you to check customer identities and beneficial owners against multiple sanctions lists including those maintained by the United Nations, the European Union, and the United States Office of Foreign Assets Control.

Ongoing monitoring represents an obligation many founders underestimate. KYC is not a one-time event occurring during onboarding. You must continuously monitor customer transactions, updating your risk assessments as behaviour changes. A customer whose transaction patterns suddenly shift to suspicious activity must trigger investigation and potentially escalation to financial intelligence units. Understanding what fintech regulation requires helps you structure your compliance programme to meet these ongoing obligations. Different regulators demand different reporting frequencies, documentation standards, and investigation protocols, meaning your compliance infrastructure must be flexible enough to accommodate multiple jurisdictional requirements. When you operate across multiple markets, centralised documentation combined with jurisdiction-specific procedures creates operational efficiency whilst ensuring local regulatory compliance.

Pro tip: Implement your KYC framework using modular software that allows you to adjust risk thresholds and monitoring triggers by jurisdiction without rebuilding your entire compliance programme.

Implementing KYC: Key Steps and Technology

Building a functional KYC system requires moving beyond policy documents into practical implementation. Your onboarding flow must begin with digital identity verification, capturing government-issued identification documents and cross-referencing them against official databases to confirm authenticity. This step alone eliminates many fraudulent entries before they enter your system. Next comes biometric verification, where customers provide facial biometrics that are compared against their identity documents using liveness detection technology. Liveness detection prevents bad actors from submitting photographs or deepfake videos instead of genuine live verification. These initial steps create a robust foundation, but they’re only the beginning. Your system must then conduct sanctions screening, checking customer identities and beneficial owners against multiple international watchlists maintained by OFAC, the UN, the EU, and other regulatory bodies. Finally, continuous monitoring must track all customer transactions after onboarding, flagging suspicious patterns that suggest money laundering, fraud, or other financial crimes. Each step must be documented with audit trails showing when verification occurred, which data was checked, and what results were obtained.

Technology accelerates KYC implementation substantially when deployed strategically. Implementing KYC involves digital onboarding processes including document checks and biometric verification powered by artificial intelligence and machine learning algorithms. AI-driven systems can verify documents in seconds, comparing security features, detecting forgeries, and extracting data automatically rather than requiring manual review. Machine learning models identify suspicious transaction patterns that humans might miss, flagging transactions for investigation without creating excessive false positives that waste compliance resources. Video verification technology allows customers to complete KYC remotely, eliminating the need for in-person visits that slow onboarding and create poor customer experience. Your technical architecture must integrate these components seamlessly. A customer should move from document upload to biometric verification to sanctions screening without manual intervention between steps, receiving real-time confirmation of success or clear guidance on remediation if verification fails.

The practical reality of KYC implementation is that automation must be balanced with human oversight. Approximately 70-80% of customer onboarding can be fully automated for low-risk customers, but edge cases require compliance officer review. A customer whose document verification fails three times, whose biometrics cannot be confirmed, or whose transaction patterns match known sanctions evasion techniques cannot be automatically approved. Your system must route these cases to humans with clear audit trails explaining why automated approval failed. For fintech startups seeking licensing in Georgia, Seychelles, or Anjouan, demonstrating this balance is critical. Regulators want evidence that you’ve invested in automation where appropriate but haven’t created a compliance programme that rubber-stamps approvals without human judgment. Data security is non-negotiable. All customer documents, biometric data, and transaction records must be encrypted both in transit and at rest, with access restricted to authorised compliance personnel. Your infrastructure must comply with data protection regulations in all jurisdictions where you operate, meaning that European customers’ data must meet GDPR standards whilst customer data in other regions meets local requirements.

Scalability shapes technology decisions fundamentally. A system that works beautifully for 100 customers monthly may collapse when processing 10,000. Cloud-based solutions from vendors like Sumsub, Onfido, or IDology offer pre-built KYC infrastructure that scales automatically, allowing you to focus on compliance policy rather than infrastructure management. Alternatively, custom development provides maximum flexibility but requires ongoing investment in maintenance and updates as regulations change. Many scaling startups begin with vendor solutions, then transition to custom systems once they’ve achieved product-market fit and can justify engineering investment. Your technology stack should support risk-based tiering, allowing you to apply different verification rigour to different customer segments. A customer depositing £500 monthly receives different scrutiny than one depositing £500,000 daily. Your system must codify these risk tiers explicitly, documenting which verification steps are mandatory for each tier and which are optional based on risk profile.

Pro tip: Start with vendor-provided KYC solutions rather than custom development, allowing you to launch compliant operations quickly whilst you focus on building product-market fit; transition to custom systems only once regulatory requirements or scale demands justify the engineering investment.

Risks, Costs, and Common KYC Challenges

KYC implementation sounds straightforward until you attempt it at scale. The reality for compliance officers at fintech startups is that KYC creates substantial operational costs whilst simultaneously introducing friction that drives customers away. Manual review processes, which many startups inherit from traditional banking, consume thousands of pounds monthly in compliance staff salaries whilst processing customers at glacial speed. A customer completing KYC in five minutes using automated systems might require forty five minutes if your process relies on manual document review. That time difference translates directly into customer drop-off rates. Studies show that every additional minute added to onboarding increases abandonment by 2-3%, meaning a forty minute process loses roughly 30-40% of initiated applications before completion. Beyond the time cost, false positive rates in fraud detection create secondary problems. Overly sensitive systems flag legitimate customers as suspicious, requiring manual investigation that consumes compliance resources without preventing actual fraud. Underly sensitive systems miss genuine threats, exposing your business to regulatory action and reputational damage. Finding the right calibration between sensitivity and false positives demands continuous tuning as fraud patterns evolve.

Common KYC challenges in fintech include over reliance on manual processes and high false positive rates that demand investment in automation and artificial intelligence. Regulatory complexity compounds these challenges substantially. A fintech operating in Georgia faces different KYC thresholds than one in Seychelles or Anjouan, yet the same customer might use accounts in multiple jurisdictions simultaneously. Your systems must track these jurisdictional variations without creating operational chaos. If you adjust KYC procedures for Georgian regulatory requirements, those changes must not inadvertently weaken your Seychelles compliance posture. Synthetic identity fraud represents a particularly insidious challenge that most startups underestimate. Unlike identity theft where criminals use real people’s stolen documents, synthetic identities combine real and fabricated information to create fictional persons who pass initial KYC checks. A customer might submit a genuine passport combined with a fabricated bank statement and utility bill, passing document verification whilst remaining entirely fictional. Detecting synthetic identities requires cross-referencing information across multiple data sources, comparing transaction patterns to claimed background, and flagging inconsistencies that simple document checks would miss.

Data quality deteriorates as your customer base scales, creating a secondary cost burden. Incomplete customer information, inaccurate addresses, or mismatched identity documents require manual remediation. A customer who uploads a blurry passport photo that cannot be read must either resubmit or remain in a suspended state, creating negative experience whilst consuming compliance resources. Balancing conversion rates with risk management introduces strategic tension that founders must navigate explicitly. A permissive KYC process that approves customers quickly maximises onboarding conversion and user satisfaction, but invites financial crime that regulators will penalise heavily. A restrictive KYC process that requires extensive documentation minimises fraud risk but rejects legitimate customers and damages growth metrics. Neither extreme serves your business. The solution requires documented risk appetite decisions showing that you’ve thought through this trade-off explicitly. Your compliance manual should specify acceptable false positive rates, maximum acceptable review times, and approval thresholds by customer segment, demonstrating to regulators that you’ve made intentional choices rather than defaulting to either extreme.

The table below compares common KYC challenges with effective solutions fintechs can adopt:

Challenge | Why It Matters | Effective Solution |

High manual effort | Slows onboarding, increases costs | Invest in AI-driven automation |

High false positive rate | Loses genuine customers, wastes resources | Fine-tune fraud detection algorithms |

Regulatory variations | Compliance gaps across markets | Implement adaptable, modular systems |

Synthetic identity fraud | Circumvents basic checks, enables crime | Cross-verify data sources for reliability |

Slow process deters users | High customer drop-off risk | Streamline checks, reduce required data |

Rapidly changing regulations add another layer of complexity. The regulatory environment for cryptocurrency, cross-border payments, and high-risk fintech services evolves constantly, with new requirements emerging from FATF, individual regulators, and international bodies. A KYC system built around yesterday’s regulatory requirements may be inadequate against today’s standards. This reality demands that your technology stack prioritises flexibility. Vendor-provided KYC solutions allow regulators to update verification requirements without forcing you to rebuild infrastructure, whereas custom systems require engineering effort every time regulations change. The costs of non-compliance dwarf the operational costs of robust KYC systems. Regulatory fines for KYC failures routinely reach millions of pounds, licence revocation eliminates your business model entirely, and reputational damage makes fundraising and customer acquisition exponentially harder. A £50,000 annual investment in KYC automation prevents £5,000,000 in regulatory fines with far greater probability than the alternatives.

Pro tip: Measure your actual onboarding drop-off rates and false positive costs explicitly, then use these figures to justify automation investments to your financial leadership by showing the return on investment through reduced friction and compliance risk mitigation.

Strengthen Your Fintech Compliance Framework with Expert Legal Support

Navigating the complex landscape of KYC requirements is a major challenge for fintech startups looking to establish trustworthy and legally compliant operations. From implementing thorough Customer Identification Programmes (CIP) and Customer Due Diligence (CDD) to managing high-risk Enhanced Due Diligence (EDD), the regulatory burdens can feel overwhelming. Ensuring your KYC process is robust, risk-based, and adaptable across jurisdictions such as Georgia, Seychelles, Curaçao, or Anjouan is crucial to prevent financial crime and obtain the necessary licenses without costly delays.

Do not let compliance complexities slow your growth or jeopardise your licence applications. Partner with NUR Legal, specialists in fintech licensing and global compliance, who provide tailored legal consultancy and support designed for high-risk regulated industries. Benefit from our proven expertise in securing crypto licences, gaming licences, and crafting bespoke compliance strategies that align with evolving FATF standards and local regulations. Take control of your onboarding procedures, customer risk assessments, and regulatory reporting now. Visit NUR Legal to start building a compliant, scalable fintech operation built on trust and legal certainty.

Frequently Asked Questions

What is the purpose of KYC in fintech?

KYC, or Know Your Customer, is a verification process used by financial institutions to confirm the identities of their customers. It aims to prevent fraud, money laundering, and other financial crimes by ensuring that only legitimate customers have access to services.

How does the KYC process work in fintech?

The KYC process typically involves three main components: Customer Identification Program (CIP), which verifies the identity of customers; Customer Due Diligence (CDD), which assesses their risk profile; and Enhanced Due Diligence (EDD), which applies stricter scrutiny to high-risk clients.

What technology is used to enhance KYC processes in fintech?

Fintech companies often use technologies such as artificial intelligence and biometric verification to streamline KYC processes. These technologies help to automate identity verification, reduce manual review times, and improve the accuracy of customer assessments.

Why is ongoing monitoring important in KYC procedures?

Ongoing monitoring is crucial as customer behaviours can change over time. Continuous scrutiny of customer transactions ensures that any suspicious activities are detected promptly, allowing institutions to update risk assessments and remain compliant with regulations.

Recommended

Comments